The best time to buy a foreclosure is before it becomes one. Once a property reaches the sheriff sale or auction stage, you are competing with other investors on price alone. But in the weeks and months between a foreclosure filing and the sale date, there is a window where a motivated homeowner still has the legal right to sell. That window is where pre-foreclosure investors build their businesses.

Pre-foreclosure investing is not about taking advantage of people in difficult situations. Done right, it is about offering a solution that genuinely helps. The homeowner avoids the damage of a completed foreclosure on their credit. They may walk away with cash in their pocket. And the investor acquires a property at a price that makes the deal work. It is one of the few strategies in real estate where both sides can legitimately win.

What Pre-Foreclosure Means

A property enters pre-foreclosure when the lender files a formal legal action to repossess it due to non-payment. In judicial foreclosure states like Indiana, this means a complaint is filed with the county court. In non-judicial states, a notice of default or notice of trustee sale is recorded.

The key point is that a pre-foreclosure property has not been sold yet. The homeowner still owns it. They can still sell it to a private buyer, pay off the delinquent amount, or negotiate with the lender. The court process takes months, and during that time, the door is open for investors who know how to find these properties and make contact.

Why Pre-Foreclosure Sellers Are Motivated

Understanding the psychology of a pre-foreclosure seller is essential to working this lead type effectively. These homeowners are dealing with several overlapping pressures.

Financial distress. They fell behind on payments for a reason. Job loss, medical bills, divorce, or a combination of factors. The financial strain is real, and it is not getting better. Most homeowners in foreclosure have been struggling for months before the filing happens.

Legal pressure. The court process has started, and ignoring it does not make it stop. Every notice, every hearing date, every piece of mail from the lender's attorney creates urgency. The homeowner knows the clock is running.

Credit consequences. A completed foreclosure stays on a credit report for seven years and makes it extremely difficult to buy another home, rent in many markets, or access credit at reasonable rates. Selling the property before the foreclosure completes can mitigate some of this damage.

Emotional exhaustion. By the time most homeowners receive the foreclosure complaint, they have already been dealing with collection calls, past-due notices, and financial stress for months. Many are simply tired and want it to be over. A clear, simple path to resolution is exactly what they need.

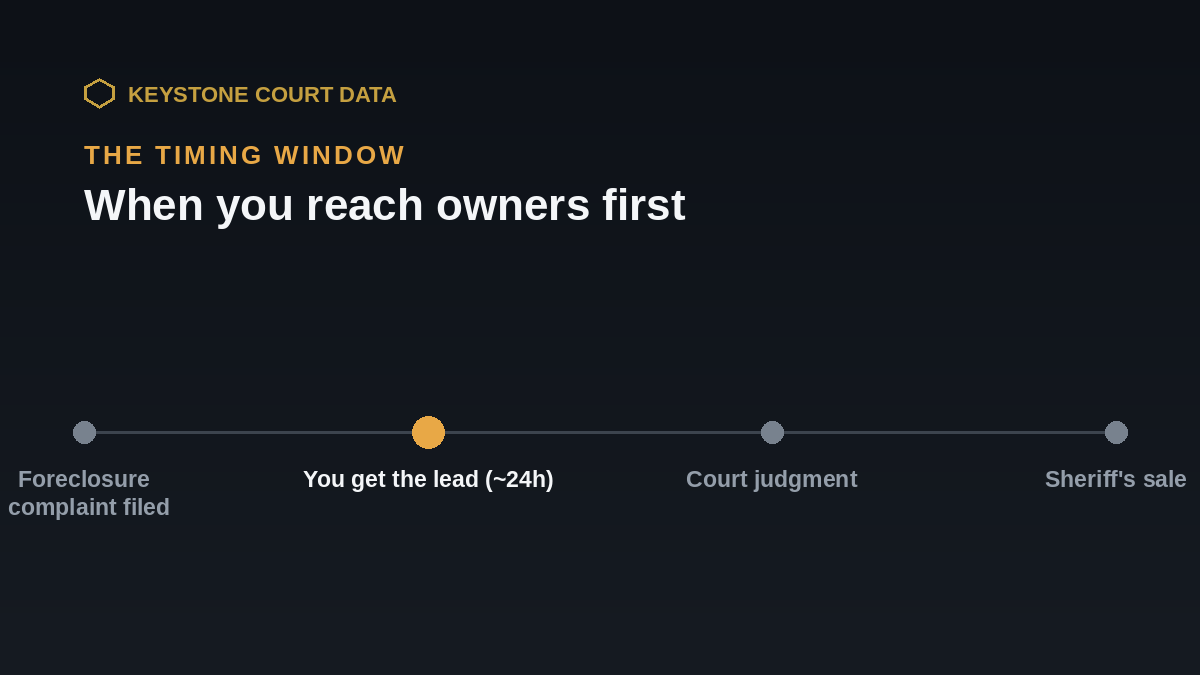

The Window of Opportunity

The pre-foreclosure window varies by state and by case, but in Indiana, the typical timeline from complaint to sheriff sale is five to ten months. That is a significant amount of time to identify leads, make contact, negotiate, and close.

The window breaks down into phases, and each phase has different implications for your approach.

Early stage (first 30 to 60 days after filing). This is the highest-value period. The homeowner has just been served and is processing what is happening. They may not realize they have options. Reaching them now, before other investors and before they have mentally given up, gives you the best chance at a productive conversation.

Middle stage (60 to 150 days). The case is progressing through the court system. The homeowner may have received a default judgment or be approaching a hearing. Urgency is increasing, and they are more likely to be receptive to an offer because the timeline is becoming real.

Late stage (150 days to sale). The sheriff sale date has been set. This is the most urgent phase, and deals here need to close quickly. The upside is that homeowners at this stage are extremely motivated. The downside is that time constraints limit your deal structure options and there is a risk the sale happens before you can close.

Finding Pre-Foreclosure Leads from Public Court Records

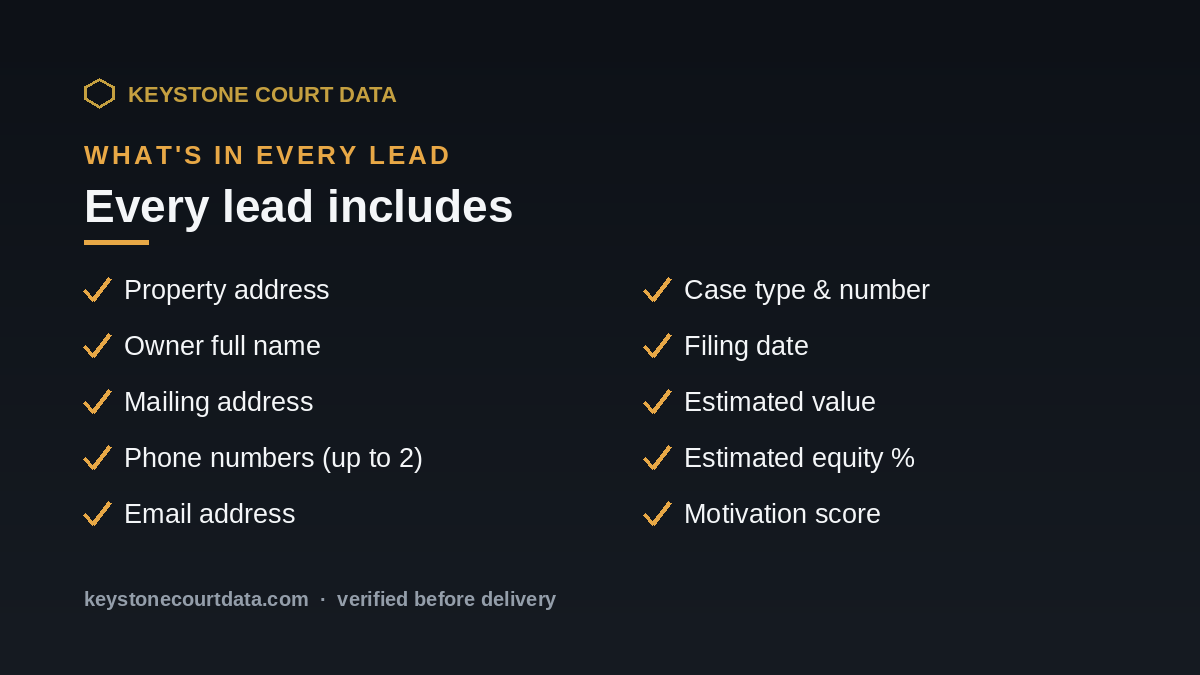

Every foreclosure filing is a public court record. When a lender files a complaint, that information becomes available through the county court system. The filing includes the property address, the borrower's name, the lender, the amount owed, and the case number.

For investors, the challenge is not whether this data exists. It is how to access it efficiently and consistently. Checking individual county court websites manually is time-consuming and easy to fall behind on. Missing a filing by a week or two can mean the difference between being first to reach a seller and being too late.

This is where a lead platform built on court records becomes essential. Keystone Court Data monitors filings across counties in Indiana, New Jersey, and Pennsylvania and delivers verified pre-foreclosure leads with property data, owner contact information, equity estimates, and motivation scoring. Instead of spending hours on courthouse research, you spend that time on outreach and deal negotiation.

Counties like Lake County, St. Joseph County, Vanderburgh County, and Clark County in Indiana produce consistent pre-foreclosure volume, making them strong markets for this strategy.

Outreach Best Practices

How you contact pre-foreclosure homeowners matters as much as when you contact them. The wrong approach gets your letter thrown away and your calls blocked. The right approach opens a conversation that leads to a deal.

Start with direct mail. A personalized letter is less intrusive than a phone call and gives the homeowner time to consider your offer. Avoid anything that looks like junk mail. Use a hand-addressed envelope, a short letter, and a clear message: you are a local investor, you saw the filing, and you may be able to help if they are interested in selling.

Follow up by phone. If you have the homeowner's phone number, call three to five days after your letter arrives. Reference the letter so they know who you are. Keep the conversation focused on their situation and what they need, not on what you want to buy.

Be consistent, not aggressive. Most pre-foreclosure deals close after multiple touches. A system that follows up every two weeks over 60 to 90 days will convert leads that a single letter or call would miss. The key is being persistent without being pushy. Every touchpoint should offer value, not pressure.

Know when to step back. If a homeowner tells you they are not interested, respect that. Continuing to call after a clear "no" damages your reputation and can create legal issues. Note the response in your CRM and move on to the next lead.

Deal Structures for Pre-Foreclosure Properties

Pre-foreclosure deals are not one-size-fits-all. The right structure depends on the homeowner's equity position, the amount owed, and the timeline.

Cash purchase. The simplest and fastest option. You make a cash offer, close in 10 to 21 days, and the proceeds pay off the mortgage. This works best when the homeowner has equity and the purchase price covers the outstanding debt plus closing costs. The homeowner walks away with cash and a clean break.

Short sale. When the homeowner owes more than the property is worth, a short sale is an option. You negotiate with the lender to accept less than the full payoff amount. Short sales take longer to close because lender approval is required, but they can produce excellent deals on underwater properties. The homeowner avoids the full impact of foreclosure on their credit.

Subject-to. In a subject-to deal, you purchase the property and take over the existing mortgage payments without formally assuming the loan. The original borrower remains on the mortgage, but you own the property. This works well when the existing loan terms are favorable and the homeowner just needs someone to take the payments off their hands. This structure requires clear communication and a written agreement that both parties understand.

Lease-option or owner financing. Less common in pre-foreclosure situations, but possible when the homeowner has equity and is open to creative terms. These structures can work for investors who want to acquire properties with minimal cash out of pocket.

Why Speed and Verified Data Matter

Pre-foreclosure investing is a speed game. The first investor to reach a motivated seller with a credible offer wins the deal. Coming in second means you spent time and money on outreach with nothing to show for it.

Speed requires two things: timely leads and accurate data. If you are working from stale filings or incomplete records, you are already behind. If your lead shows one property address but the homeowner actually lives at a different mailing address, your direct mail never arrives. If the phone number is wrong, your calls go nowhere.

Verified data, the kind that includes confirmed property details, current mailing addresses, working phone numbers, and up-to-date case status, is what separates productive pre-foreclosure campaigns from wasted effort. When you combine verified data with motivation scoring that tells you which leads are most likely to convert, you can focus your time on the highest-probability opportunities instead of working the entire list blindly.

Pre-foreclosure investing rewards discipline and consistency. Build a system that delivers new leads weekly, reach out promptly, follow up consistently, and structure deals that work for both you and the seller. The investors who do this well build deal flow that others cannot replicate.

Ready to start? Request a free trial to see pre-foreclosure leads across Indiana counties with complete property data, owner contact information, and motivation scoring. Or view county subscription pricing to lock in your markets.