Indiana is a judicial foreclosure state. That single fact shapes everything about how foreclosures work here and, more importantly, where the opportunity lies for real estate investors. Unlike states where foreclosures happen outside the court system through a trustee process, every Indiana foreclosure must go through the courts. That means public filings, predictable timelines, and clear windows for investors to reach motivated sellers.

If you invest in Indiana real estate, understanding the foreclosure timeline is not optional. It is the foundation of a successful pre-foreclosure strategy. Knowing where a homeowner sits in the process tells you how motivated they are, how much time they have, and what deal structures are realistic.

The Indiana Foreclosure Timeline: Step by Step

The foreclosure process in Indiana follows a defined legal sequence. While individual cases vary in duration, the overall structure is consistent across all 92 counties. Here is how it plays out.

Step 1: Default and Pre-Filing (30 to 90 days). The process starts when a borrower falls behind on mortgage payments. Most lenders will not take action after a single missed payment. Typically, a borrower needs to be 60 to 90 days delinquent before the lender initiates formal proceedings. During this period, the lender may send demand letters and attempt to work out a payment plan. There is no public filing at this stage.

Step 2: Complaint Filed (Day 1 of the court process). The lender files a foreclosure complaint with the county court. This is the moment the case becomes a public record. The complaint names the borrower, identifies the property, and states the amount owed. This filing is the earliest point at which investors can identify the property as a pre-foreclosure lead. In high-volume counties like Lake County and St. Joseph County, new complaints are filed weekly.

Step 3: Service of Process (10 to 30 days after filing). The borrower must be formally notified of the lawsuit. This happens through personal service by a sheriff or process server, or through publication if the borrower cannot be located. The borrower then has 20 days to file a response. Most homeowners in foreclosure do not hire an attorney or file a formal response, which accelerates the timeline.

Step 4: Default Judgment or Response (20 to 60 days). If the borrower does not respond within 20 days, the lender can request a default judgment. If the borrower does respond, the case proceeds through the litigation process, which adds time. In practice, most residential foreclosures in Indiana result in default judgments because the borrower does not contest the action.

Step 5: Court Hearing and Judgment (30 to 90 days). The court reviews the case and issues a judgment of foreclosure. This judgment authorizes the sale of the property to satisfy the debt. The court also sets a sale date. Indiana law requires that the sale be scheduled no sooner than 30 days after the judgment. This hearing stage is where cases can stall, particularly in courts with heavy dockets. Counties like Vanderburgh County and Clark County process these cases on predictable schedules.

Step 6: Sheriff Sale (30+ days after judgment). The property is sold at a public auction conducted by the county sheriff. The opening bid is typically the amount owed on the mortgage. If no one bids above the minimum, the lender takes the property back as an REO (real estate owned). In Indiana, there is no statutory right of redemption after the sheriff sale for most residential properties, which means the sale is final.

Total timeline: 150 to 300 days from complaint to sheriff sale. The typical Indiana foreclosure takes five to ten months from the initial filing to the completed sale, though contested cases or court delays can extend this further.

Where Investors Fit In: The Pre-Foreclosure Window

The period between the complaint filing (Step 2) and the sheriff sale (Step 6) is the pre-foreclosure window. This is where investors have the greatest opportunity. The homeowner knows they are losing the property. The legal process is already in motion. And the clock is ticking.

The early part of the window, immediately after the complaint is filed, is the most valuable. At this point, the homeowner still has time to sell the property voluntarily. They may have equity in the home. And they are often more receptive to a conversation about selling because they have not yet fully processed what is happening.

As the case progresses toward judgment and sheriff sale, the homeowner's options narrow. But even late in the process, deals are possible. Short sales, subject-to arrangements, and cash purchases can all close before the sale date if both parties move quickly.

What Data Is Available from Court Filings

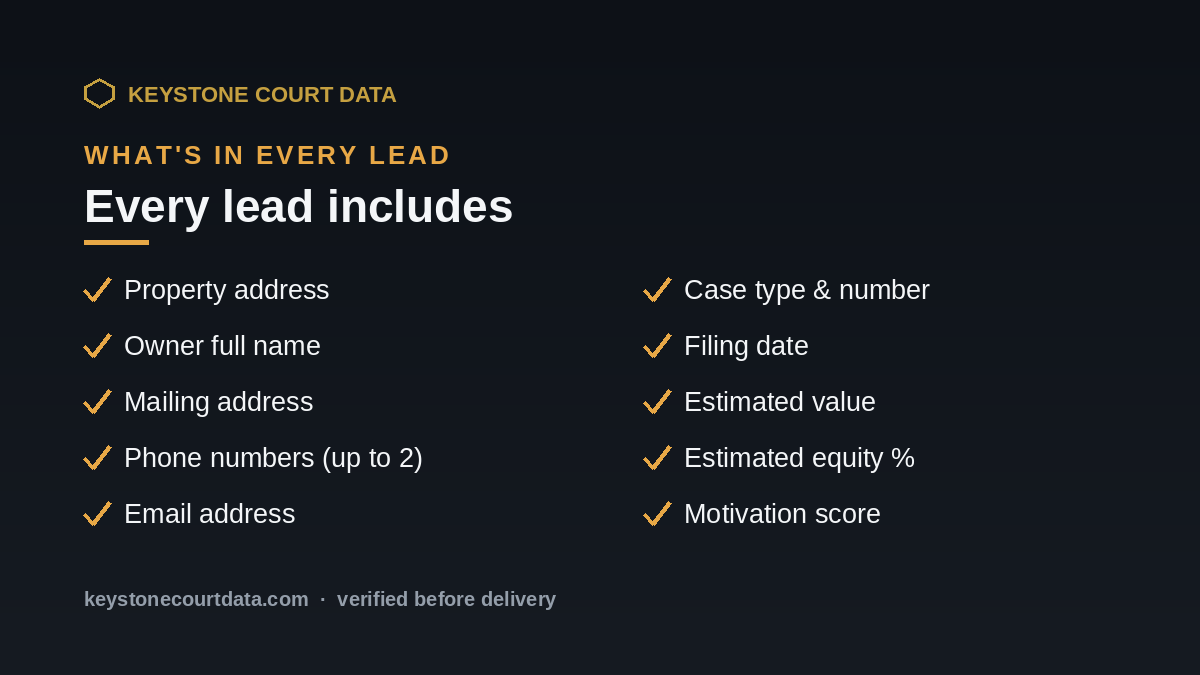

Indiana foreclosure filings are public records, and they contain a significant amount of useful information for investors. A typical filing includes:

- The property address and legal description

- The borrower's name (and any co-borrowers)

- The lender and their attorney

- The amount owed, including principal, interest, and fees

- The case number and filing date

- The current case status and upcoming hearing dates

When combined with property data like estimated value, equity percentage, and owner contact information, these filings give investors everything they need to evaluate a potential deal and reach the homeowner. Keystone Court Data packages this information into verified leads with motivation scoring, so you can prioritize the leads most likely to convert.

How to Approach Pre-Foreclosure Homeowners

Reaching out to someone facing foreclosure requires a careful balance of urgency and empathy. These homeowners are dealing with real financial stress, and the last thing they need is a hard sell. The investors who convert the most pre-foreclosure leads are the ones who lead with solutions rather than offers.

Be direct about why you are reaching out. Homeowners know their foreclosure is a public record. Pretending otherwise damages trust. A straightforward approach works: you saw the filing, you buy properties in the area, and you want to explore whether a sale might be a better outcome than going through with the foreclosure.

Explain the benefits of selling before the sale. Many homeowners do not realize they have options. Selling before the sheriff sale lets them protect whatever equity remains, avoid a foreclosure on their credit report (if the sale satisfies the debt), and control the timeline rather than having it dictated by the court.

Move quickly once you have engagement. If a homeowner is willing to talk, do not let weeks go by. Get the property under contract, work with a title company, and close as fast as possible. Time is the enemy of every pre-foreclosure deal.

Offer multiple options. Not every deal needs to be a cash purchase at 60 cents on the dollar. Subject-to deals, where you take over the existing mortgage payments, can be attractive to homeowners who owe more than the property is worth. Short sales, where the lender agrees to accept less than what is owed, are another option for underwater properties.

Using the Timeline to Your Advantage

The best pre-foreclosure investors in Indiana treat the timeline as their strategic framework. They know that a filing from last week is a warmer lead than a filing from three months ago. They know that a case approaching judgment needs a faster close. And they know which counties, like Lake County, Hendricks County, and St. Joseph County, have court schedules that create predictable windows of opportunity.

Building a system that tracks filings across multiple counties, identifies the strongest leads, and triggers outreach at the right moment is what separates occasional deal-finders from consistent investors. Court records are the raw material. Your outreach system and speed of execution turn those records into closed deals.

Start reviewing pre-foreclosure filings in Indiana counties today. Request a free trial to see verified leads with complete property data, owner contact information, and motivation scoring. Or view pricing to explore county subscription options.